All about matching funds

Market interest rates have been very low for years. Interest rates have been rising since 2021. In 2022, interest rates rose dramatically in one year. Since then, interest rates have been going down and up in small steps. To keep your expected pension stable, we use matching funds. We explain how this works.

If you are about to retire, you will see that your pension capital decreases. This is because we increasingly invest in matching funds as you get older. We don’t just do that. We have a good reason for that. Because as crazy as it may sound, it keeps your pension as stable as possible. This animation explains how matching funds work in less than 2 minutes. Or read the explanation below the animation.

Your pension capital is invested

Your employer has opted for a BeFrank pension scheme. At BeFrank we invest your pension capital. Because, in the long run, returns on investments are nearly always higher than for savings. However, investing also always involves risks. We limit the risk for your pension capital by using a broad spread of investments. We also lower your risks as you get older. We do this by increasingly investing in matching funds.

Good to know: you also have influence on how much risk you take with your pension capital. Fill in the Profile Selector and see which investment risk suits you best. Done quickly!

Matching funds provide stability

How do matching funds work? When you retire, you purchase a pension. You will receive that for life. The amount of your final pension depends on the amount of your pension capital, but also on the interest. We cannot predict whether interest rates will rise or fall when you purchase your pension. Nevertheless, we want to prevent your expected pension benefit from fluctuating a lot as you approach your retirement age. That is why we increasingly invest your pension in matching funds as you get older. Because matching funds react opposite to interest rates. This way we keep your expected pension benefit solid.

How does this work?

- If the interest rate falls, you can purchase a lower pension with your pension capital. So you need more capital for the same pension. Matching funds react in the opposite direction to interest rates and in this case provide a higher return. So you still purchase approximately the same pension.

- If the interest rate rises, you can purchase a higher pension with your pension capital. So you need less capital for the same pension. Matching funds react in the opposite direction to the interest rate and in this case provide less return. So you still purchase approximately the same pension.

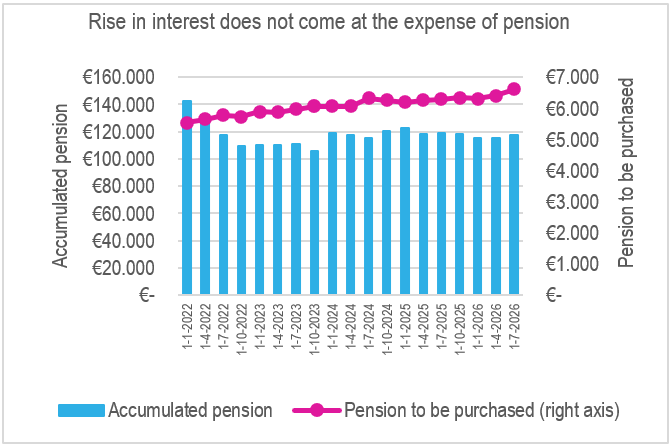

Example calculation:

amount of capital and pension to be purchased in graphs

| Date | Development capital | Gross pension to be purchased (annual amount) | 10-years interest |

|---|---|---|---|

| 1-1-2023 | € 110.109,02 | € 5.882,55 | 3,11% |

| 1-4-2023 | € 110.440,17 | € 5.876,57 | 3,01% |

| 1-7-2023 | € 110.951,37 | € 5.960,74 | 2,99% |

| 1-10-2023 | € 105.420,78 | € 6.053,97 | 3,50% |

| 1-1-2024 | € 118.851,54 | € 6.057,65 | 2,41% |

| 1-4-2024 | € 117.719,63 | € 6.069,77 | 2,57% |

| 1-7-2024 | € 115.423,37 | € 6.314,29 | 2,79% |

| 1-10-2024 | € 120.711,52 | € 6.258,11 | 2,37% |

| 1-1-2025 | € 122.576,39 | € 6.198,49 | 2,37% |

| 1-4-2025 | € 118.369,56 | € 6.259,79 | 2,67% |

| 1-7-2025 | € 118.773,40 | € 6.283,21 | 2,61% |

| 1-10-2025 | € 117.983,55 | € 6.334,48 | 2,70% |

| 1-1-2026 | € 115.056,08 | € 6.311,22 | 2,97% |

| 1-4-2026 | € 115.364,48 | € 6.404,94 | 3,12% |

| 1-7-2026 | € 117.755,30 | € 6.613,01 | 2,93% |