Investing at BeFrank

Freedom of choice for employees

At BeFrank, we invest 100% of the pension contributions made by employees. Your customer and staff can make some choices for themselves. This page explains how investing at BeFrank works.

At BeFrank, we invest using the lifecycle method. This means we take an employee’s age into account. The closer they come to their retirement age, the less investment risks we take.

In short: we go for returns where we can and for certainty as an employee approaches their pension age.

Staggered investment

We invest pension capital in companies, sectors and investment categories (equities and bonds) across the world. That way, we limit investment risks.

Choices for your customers

At BeFrank, your customers choose their own lifecycle from three different forms of investment: passive, active and sustainable. They also select one of five risk profiles: very defensive, defensive, neutral, offensive and very offensive. After that, employees decide whether those choices still suit them.

Want to find out more? We have listed the investment choices for employers.

Freedom of choice for employees

At BeFrank, employees are in charge of their own pension. And that’s only logical. After all, it’s their future at stake.

Employees can therefore decide whether they agree with the decisions made by their employer. They may want to make changes so that the lifecycles match their personal situation better. They can do this at any time.

Employees also decide whether they want to continue investing part of their pension capital after their retirement date. If they want more freedom, Do It Yourself investing may be an interesting option. However, your customer does need to allow this.

Notifying changes

If an employee want to make a change, they can do this through their personal pension page in a few simple steps.

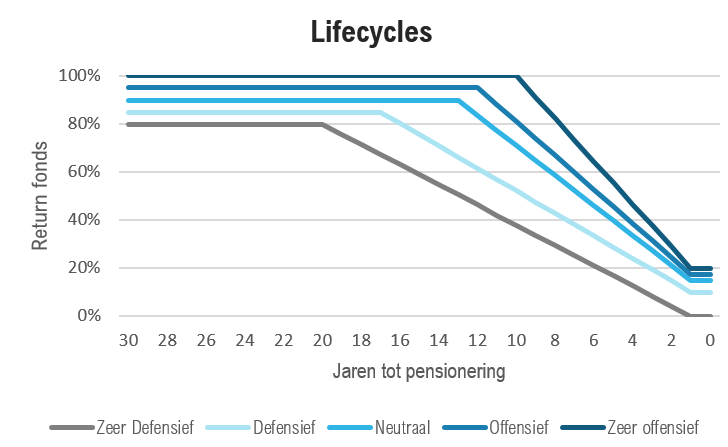

Risk reduction

At BeFrank, we take employees’ ages into account. If an employee is approaching their retirement age, we limit risky investments where possible. This gives employees increased certainty about their final pension benefits.

Employees can also have their investment risks reduced at a faster or slower rate. The graph below shows how this works.

If an employee wants to reduce their risk, they can select their own risk profile and:

1. Their risk reduction age

By default, we reduce risky investments until employees’ (expected) State Pension Age. If an employee wants to change this, they could choose the retirement age in their pension scheme as their final age for risk reduction.

2. The risk reduction rate

Where possible, we gradually reduce investment risks. The employee can decide by how much we reduce the risks: by 15%, 30%, 45% or 60%, for example (the choices depend on the risk profile).

Good to know: the longer we invest with high risk, the higher the chance that the pension capital will grow. However, there is also a chance that your pension could realise greater losses.